Sunday Reads #153: How LUNA crashed from USD 40 billion to zero. Overnight.

What a cryptocurrency's death spiral teaches us about the nature of risk.

Hey there!

For folks who’ve joined over the last few days, sharing a couple of links that you might like:

Step by step, ferociously - looking back at 2021.

On to this week’s newsletter.

I don't know if you've been following the latest drama in crypto. The USD 40B+ ecosystem of the Terra blockchain (which had the UST stablecoin and the LUNA token) collapsed to zero overnight.

Total carnage, yes. But it also highlights how "risk" actually works.

Autopsy of a death spiral.

Before we dig into what happened, What are Terra and LUNA exactly?

In brief: The Terra blockchain powered the token called UST, which is supposed to track the US Dollar. 1 UST = 1 USD (at least in theory).

It's called a stablecoin, because its value is pegged to - and is therefore stable versus - the US dollar.

It used another token - called LUNA - to ensure this stability. Won't go into the details of the mechanism here; you can google it if you're interested.

On Mon May 9, 1 UST was worth 1 USD. On Friday the 13th (if ever there was an omen!), it was worth zero.

If anything, LUNA had an even steeper fall.

An absolute bloodbath. LUNA and UST were very popular (I never bought any, but i know a lot of folks who were holding both tokens).

What happened?! How can so much value evaporate in an instant!

Turtles all the way down.

There's a hilarious anecdote at the beginning of Stephen Hawking's A Brief History of Time. I read it as a kid, and I still remember it:

A well-known scientist (some say it was Bertrand Russell) once gave a public lecture on astronomy.

He described how the earth orbits around the sun and how the sun, in turn, orbits around the centre of a vast collection of stars called our galaxy.

At the end of the lecture, a little old lady at the back of the room got up and said: "What you have told us is rubbish. The world is really a flat plate supported on the back of a giant tortoise."

The scientist gave a superior smile before replying, "What is the tortoise standing on?"

"You're very clever, young man, very clever," said the old lady. "But it's turtles all the way down!"

I was reminded of this by the crash of LUNA and Terra.

To a certain degree, stablecoins run on trust. Trust that one token of that stablecoin will always be equal to one US Dollar.

But look a little closer and you realize - trust is all they run on.

It's trust all the way down.

As I said in There ain't no such thing as a free lunch in Jul 2021, but about Tether (another stablecoin):

The biggest risk to the current crypto wave is, ironically, a stablecoin...

A crash won't happen overnight.

Whenever the USDT-USD rate moves slightly below 1:1 (e.g., 1 USD = 1.005 USDT), arbitrageurs will come in and exploit the difference. They will sell USD to buy USDT, and thereby push USDT back up to 1 USD…

Now, let's say, during an especially volatile time, the peg moves a little farther than usual. It moves to 1 USD = 1.2 USDT, say.

What happens then?

If it's "common knowledge" that USDT isn't collateralized enough (i.e., everyone knows, and everyone knows that everyone else knows), then the trust is broken.

You know what happens next. A flight to safety.

Investors see the widening USDT-USD gap as proof the peg won't be maintained, and start selling USDT.

This pushes the price of USDT down even further. Driving more investors to panic-sell.

And so on.

Feedback loops are a fearsome thing. In a flash, the peg disintegrates.

Tether has at least some collateral backing its stablecoin USDT. But Terra is an “algorithmic stablecoin”. It has no collateral at all!

Instead, it depends on its algorithm and the "invisible hand" of the markets to maintain its peg to the US Dollar.

This is a good thread on what exactly happened with LUNA and Terra.

It was a textbook crash.

A hacker triggers a movement of the peg → people lose some confidence → peg moves some more → people lose more confidence → Repeat until zero.

But this story also illustrates another point about the nature of risk.

What you know for sure...

In "risky" asset classes, risk is expected.

When it shows up uninvited to your party, you're unhappy. But you understand.

Yes, investing in Bitcoin is risky. It could go down by 20% in a day.

And when it goes down by 30%, you say "OK, I knew it was risky".

You feel sad, frustrated, defeated. But you knew the deal going in.

In "safe" asset classes, risk is zero. Until it shows up.

When it shows up to your party uninvited, your response isn't "Damn it, why are you here?".

Instead, you're shrieking, "What! Didn't you die 10 years ago?". And then you black out.

A safe asset is either worth 100 (if it's indeed safe), or it's worth 0 (if you were wrong about it being safe).

As Matt Levine said in Money Stuff, "Safe assets are much riskier than risky ones".

This is I think the deep lesson of the 2008 financial crisis, and crypto loves re-learning the lessons of traditional finance.

Systemic risks live in safe assets. Equity-like assets — tech stocks, Luna, Bitcoin — are risky, and everyone knows they’re risky, and everyone accepts the risk. If your stocks or Bitcoin go down by 20% you are sad, but you are not that surprised. And so most people arrange their lives in such a way that, if their stocks or Bitcoin go down by 20%, they are not ruined.

On the other hand safe assets — AAA mortgage securities, bank deposits, stablecoins — are not supposed to be risky, and people rely on them being worth what they say they’re worth, and when people lose even a little bit of confidence in them they crack completely.

Bitcoin is valuable at $50,000 and somewhat less valuable at $40,000. A stablecoin is valuable at $1.00 and worthless at $0.98. If it hits $0.98 it might as well go to zero.

Going back to my There ain't no such thing as a free lunch:

It all comes down to one timeless truth: There ain't no such thing as a free lunch.

… Stablecoins are useful because they are stable cryptocurrencies. Whereas all other cryptocurrencies are volatile.

It's worth asking the question - how are stablecoins removing volatility from the system?

Making a volatile asset less volatile requires energy. Where's that energy coming from? Who's paying for it?

To paraphrase Buffett, if you look around and don't see anyone paying for it, then you're paying for it.

How are you paying for the volatility? By taking on invisible risk.

The volatility isn't disappearing. It's piling up silently, in an invisible corner.

A magician can make one or two rabbits disappear into his hat. All fine. But the more rabbits that go in, the greater the risk that the false bottom will fall off. And he’ll suddenly find that the rabbits have multiplied in there.

Or, sticking with the free lunch metaphor:

The costliest lunch is the one that you thought was free, but the maitre d' presents you a bill at the end and says, "Thank you for buying my bankrupt restaurant".

Hi, I’m Jitha. Every Sunday I share ONE key learning from my work in business development and with startups; and ONE (or more) golden nuggets. Subscribe (if you haven’t) and try it out for free 👇

Golden Nugget of the week.

I enjoyed listening to Shaan Puri's conversation with Moiz Ali on the My First Million podcast.

Moiz Ali is the founder of Native, a clean deodorant brand. He sold Native to P&G in 2017 for $100M.

Lots of lessons from the podcast, but one stood out to me:

Guard your secret!

Before selling to P&G, Moiz and his team did zero PR for Native. No fawning TechCrunch pieces, no branded sweatshirts, nothing.

Heads down, silently scaling their business.

Once P&G acquired Native for 100 million, everyone realized how lucrative the space was.

And within 12 months, there were tons of "Clean" / "Parabens-free" deodorants on the market.

Reminds me, once again, of the AWS story that I mentioned in How Microsoft became a multi-trillion dollar company:

… both (Bezos) and Jassy lobbied to conceal the division’s financial details from public view, even amid the widespread skepticism that throttled the company and its stock price in 2014.

But in 2015, Amazon’s finance department argued that the division’s revenue was approaching 10 percent of Amazon’s overall sales and would eventually trigger reporting requirements under federal law.

“I was not excited about breaking our financials out because they contained useful competitive information,” Jassy admitted.

Nevertheless, that January, Amazon signaled that it would report AWS’s financial results in its quarterly report for the first time, and investors girded in anticipation.

Many analysts predicted that AWS would be revealed as just another Amazon “science project”—a lousy, low-margin business that was sapping energy from the company’s more advanced efforts in retail.

In reality, the opposite was true. That year, AWS had a 70 percent growth rate and 19.2 percent operating margin, compared to the North American retail group’s 25 percent growth rate and 2.2 percent operating margin. AWS was gushing cash, even as it rapidly consumed most of it to build even more computing capacity and keep up with the fast-growing internet companies like Snapchat that were piling onto its servers.

This reporting was a huge surprise for the analysts and investors who monitored and scrutinized Amazon, and likely even a bigger one for Microsoft, Google, and the rest of the enterprise computing world.

Bezos and Jassy knew instinctively that the moment others found out how lucrative cloud services was, they would come rushing in. And they did.

Uncertainty is a moat.

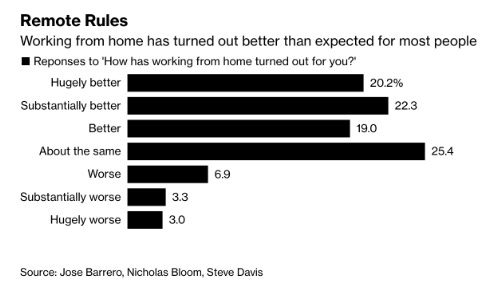

Chart of the week.

People prefer Work from Home. A LOT!

Oldie but goodie: The CIA's Rulebook to Sabotage Organizations.

A great way to improve meetings in your company is to give your colleagues this CIA manual.

Simple instruction: Just... DON'T do anything written in here.

As I've written before: the best way to do good meetings is not to do bad ones.

That’s it for this week. Hope you enjoyed it, and are staying safe, healthy and sane.

I’ll see you next week.

Jitha