Sunday Reads #127: Exhaust fumes and infinite games - how startups are valued.

And crypto's big short.

Hope you’re keeping safe and sane. It is a troubling time in many parts of the world.

Welcome to the latest edition of Sunday Reads, where we'll look at a topic (or more) in business, strategy, or society, and use them to build our cognitive toolkits for business.

If you’re new here, don’t forget to check out the compilation of my best articles: The best of Jitha.me. I’m sure you’ll find something you like.

And here’s the last edition of my newsletter, in case you missed it: Sunday Reads #126: There ain’t no such thing as a free lunch.

This week, let’s talk about startups. More specifically - how startups are valued. And what that implies for long-term success in startup investing. If you’re interested in angel investing, definitely read this.

Next, a follow up to last week’s article on Tether, the stablecoin that could cause a crypto collapse. More evidence that the music might stop soon. And some predictions on how it’ll end.

And to finish up, something that made me smile (🥇), and something that scared me ⛰ 🧗♀️.

Here's the deal - Dive as deep as you want. Read my thoughts first. If you find them intriguing, read the main articles. If you want to learn more, check out the related articles and books. Oh, and do subscribe if you haven’t 😊.

1. Exhaust Fumes and Infinite Games.

Early stage valuations aren’t really valuations. They are the exhaust fumes of a negotiation about two things — the amount raised and the amount of dilution.” — Fred Wilson.

Sajith Pai’s article ‘Exhaust Fumes’, or, Understanding Startup Valuations is a great read.

At the surface, it's about how startups are valued.

The standard way of valuing companies is Discounted Cash Flow, or DCF analysis. Or if future cash flows are quite unpredictable, then Peer Comparables.

In both cases, what you value is the potential cash flows from the business.

But startup valuation is a little meta.

Like all valuation exercises, startup valuation is a prediction. But it's not a prediction of value of future cash flows. It's a prediction of behavior.

In fact, it's a coordination game, a little like the Prisoners' Dilemma.

The twist is that the coordination happens over a period of several years.

Pai calls it long-term multi-party staging.

There are only two factors that are important in startup valuations:

How much money does the startup need to get to the next round?

How much stake do I want to hold at time of liquidity event?

As he says:

The $1m funding amount is the perceived amount thought of by the seed VC to get the startup to the next stage (Series A). The 20% equity stake is what the VC has determined as the desired target stake to hold after the initial round. Long years of investing, or market lore, has informed them that this target stake after several future rounds of dilution will result in a meaningful stake of 8–10% at the time of exit, meeting their internal exit outcomes for the startup.

How does the seed VC value the startup? Well, the answer is simple. The startup’s value is the funding amount divided by the equity stake that the startup is diluting. Hence if the startup is raising $1m = ₹7.5crs from the VC, and diluting 20% stake, then the value of the startup becomes $5m, or $1m divided by 20%. (In ₹ terms ₹37.5crs = ₹7.5crs divided by 20%).

This is how the coordination game plays out in India, in 2021 (values are higher in the US).

But this valuation "protocol" is only ostensibly what the article is about. The implications of this approach are far more interesting.

Startup investing is an "infinite game".

Given that startup investing is about coordination over years, signaling becomes paramount.

Therefore, VC firms (at least the good ones) all play long-term games. Not just with founders, but with other funds too.

Reputation is important, if only so that you get the next good deal.

That's why VCs are "founder-friendly". Not out of the goodness of their hearts.

That's why KPCB sold back their stake in Gumroad to the founder for $1. They were planning to write off the investment anyway. This way they might at least get good referrals through the founder later.

It's not about any deal standalone. It's about that deal plus enabling future deal flow.

Long-term players win more than newer ones.

Given the "infinite game" nature of startup investing, it's no surprise that long-term players win more than newer ones.

The data shows that too.

If a VC's previous fund was in the top quartile of performance, then the chances of its next fund also being in the top quartile is nearly 50%.

For a Private Equity player, the corresponding persistence is only 24%.

Coordination game + Power Law Distribution → Access is the biggest bottleneck.

We already know that VC investment is about "home runs". Many of your deals will go bust, but the ones that don't, should return big. i.e., a Power Law distribution.

As Ben Evans shows, 6% of deals produce 60% of returns, and 50% of investments lose money.

Long-term infinite game + power law → Everyone is really solving for access.

You don't win because of prescience about the future. You don't win due to an uncanny ability to pick winners. You don't win by building a tireless fundraising machine.

You win with access.

Persistent access to the best deals is the most critical leverage point in venture capital.

I've written about this in Drunkards and Streetlights:

Yes, the hardest part is finding the best companies.

Even if you're almost psychic at picking winners, you can only pick winners among the startups you see (i.e., under your streetlight).

And in a power law world, one startup makes all the difference. What if it's one you just missed investing in? That one networking dinner you missed. That one week you were on holiday. The unicorn is just 5m away from your streetlight, but completely in the dark.

And it doesn't end there. Even if you do find tomorrow's billion dollar company, so will other, bigger institutional investors. And they will have no remorse muscling you out, as Paige Craig found out with Airbnb.

This happened to me and OperatorVC. One of our startups hit a strong tailwind of growth, and we were super excited.

Guess what - we were forced to sell at 10x, because the bulge-bracket VC investing in their Series B wanted to "clear the cap table" as a precondition to invest.

Yes, 10x is not a bad return. But it's not good enough.

Given the number of failures you'll invariably see, you need your wins to be "home runs". You need them to be 30x, not 10x.

This is also why I've dialed down my angel investments a little bit. For every deal, I think hard - am I a drunkard searching under a streetlight, just because it's bright here?

2. Crypto's Big Short

After last week's newsletter on the stablecoin risk to crypto, a friend shared an older article with me: The Bit Short: Inside Crypto’s Doomsday Machine.

The author makes a very interesting case.

A. Tether is critical to trade crypto on most Centralized Exchanges.

At the time of the article, over 2/3rds of Bitcoin purchases were being made with USDT, Tether's stablecoin.

B. Believing in Tether's stability requires believing in a trusted third party. Who happens to be under investigation for fraud.

Tether and its parent Bitfinex are under active investigation by regulators in the US.

And as I mentioned in There ain't no such thing as a free lunch, despite repeated requests, Tether has been unable to provide enough assurance that it's well collateralized.

In fact, every pronouncement only makes the risk starker. For instance, here's what they said in a recent interview:

At the 12:50 mark:

We maintain cash that is many multiples above our single biggest redemption thus far, and above our biggest 24 hour period of redemptions. So we're quite comfortable with our reserves.

As I said last week, that sounds like… not much at all?

Tether's bank deposits are all in the Bahamas. And never mind Tether's accounts themselves, all the banks in the Bahamas don't have enough dollars to support Tether's stablecoins!

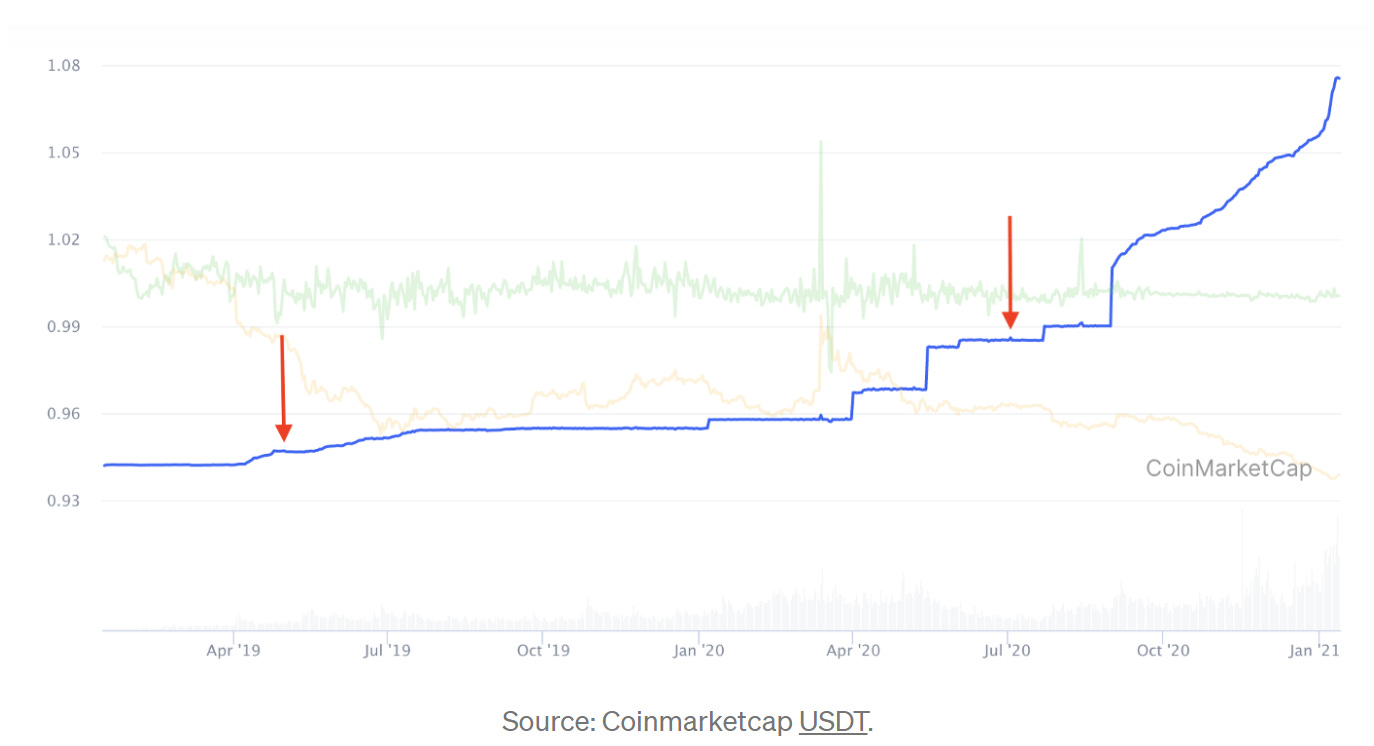

C. Tether's coin issuances have skyrocketed, as regulators have upped the pressure.

See the trend from Jul 2020 onwards.

Could this be Tether realizing that the music is going to stop soon, and might as well make the most of it?

By issuing USDT with abandon, without the dollars to back it up, Tether is in effect shorting the US Dollar. To the tune of USD 25Bn.

You know what happens next. A squeeze. Might be devastating, unlike Gamestop.

How will this end?

After last week's article, a friend asked - OK, how will this end?

My best guess:

Further reading

My post last week: There ain’t no such thing as a free lunch.

My twitter thread on the stablecoin risk. Also check out the FAQ follow-on thread.

3. This made me smile 🥇.

The Olympics are on, and so I'm suddenly interested in cycling, hockey, and athletics.

Lots of great stories there (including India winning a GOLD in Javelin throw! 🥳).

But one story that was hilarious was the road cycling event.

An unheralded contender (who happens to be a Math PhD, yes) won the race... partly because everyone else forgot she was ahead??

4. This scared me 😨

I read this paper: Evidence of brain damage after high-altitude climbing by means of magnetic resonance imaging.

The title says it all, but I'll say more anyway.

From the abstract:

We conclude that there is enough evidence of brain damage after high altitude climbing; the amateur climbers seem to be at higher risk of suffering brain damage than professional climbers.

I love climbing (not mountaineering, but multi-day treks in the Himalayas), so this scared me. And it turns out lot of people have guessed that this happens.

And from Alexey Guzey:

“"High-altitude mountaineering kills brain cells—no doubt," says RMI guide Melissa Arnot. "But this is what I do. It's my profession."

One internationally known climber confided to me that he isn't sure whether his cognitive function recovers completely after big climbs, or if he just gets accustomed to the diminished capacity.

Another, RMI guide Alex Van Steen, once told me, "Sometimes you're never quite right afterwards." “

Yikes.

That's it for this week! Hope you liked the articles. Drop me a line (just hit reply or leave a comment through the button below) and let me know what you think.

PS. I’m slowing down a little bit for the next few weeks. Will be back to weekly soon!

Until next time, wish you good health, safety, and sanity.

Jitha